Important: This site is for informational purposes only.

Nothing here constitutes financial, tax, or investment advice.

Consult a licensed financial advisor before making any investment decisions.

| Last Updated: 2026-05-16

Vault Retirement Guide evaluated seven Gold IRA companies against six operational transparency dimensions — fee disclosure, custodian relationships, depository disclosure, buyback program specificity, minimum investment accessibility, and independent ratings posture — to identify the providers most aligned with informed retirement decision-making in 2026.

Last verified: May 16, 2026 · Methodology: operational transparency · Not financial advice

This content is for informational and educational purposes only. Nothing here constitutes financial, tax, investment, or legal advice. Gold and precious metals investments carry significant risk including loss of principal.Regulatory frameworks governing retirement accounts, including ERISA and IRS rules, are complex and subject to change. References to ERISA in this guide describe the regulatory landscape as the author understands it and should not be relied upon as a definitive statement of legal requirements. Before making any rollover, contribution, or investment decision, consult a licensed financial advisor, tax professional, or ERISA-qualified specialist who can evaluate your specific circumstances. Past performance of gold or any asset class does not guarantee future results. Affiliate relationships may exist with companies discussed; see our full disclosure.

About This Guide

Who this guide is for: Investors evaluating a 401(k), 403(b), or traditional IRA rollover into a self-directed Gold IRA in 2026

What this guide covers: Seven established Gold IRA companies evaluated on six operational transparency dimensions

What this guide does not cover: Personalized financial or tax advice, market timing recommendations, or specific allocation guidance

Our differentiator: We rank companies on operational transparency — what they disclose in writing before account opening — not on marketing reach

Our 2026 evaluation framework weights operational transparency as the primary differentiation dimension. The methodology reflects an editorial position: that for an asset class held outside the traditional brokerage system, the willingness of a provider to openly disclose its operational stack is the single most informative signal of how it will treat investors over the multi-decade holding period typical of retirement accounts.

The six dimensions, in order of weighting:

1. Fee Transparency

Does the company publish a complete fee schedule before account opening? Setup fees, annual custodial fees, annual storage fees, and any transaction or wire fees. Companies that publish their fee schedule in writing on their public website score highest. Companies that disclose fees only on request score in the middle. Companies that disclose fees only after the account opening process begins score lowest.

2. Custodian Disclosure

Which IRS-approved custodian(s) does the company work with? Is the relationship clearly named on the company's site? Is the custodian's own fee schedule independently accessible? Per Internal Revenue Code Section 408, the precious metals within an IRA must be in the physical possession of a bank or an IRS-approved non-bank trustee — making the custodian a structural component of the account, not an optional detail. For IRS rules on custodian approval, purity standards, and contribution limits, see our 2026 Gold IRA guide covering IRS rules and approved metals.

3. Depository Disclosure

Which IRS-approved depository or depositories store the metals? Is segregated vs. commingled storage clearly explained? Are insurance carriers named? Approved depositories include institutions such as Brink's, Delaware Depository, International Depository Services, and CNT Depository, among others. Companies that name their depository partners openly score higher than companies that leave this vague until after commitment.

4. Buyback Program Specificity

Does the company commit in writing to a buyback program? Is the disclosed spread quantified? Is the typical settlement timeline stated? "We offer buybacks" without specifics scores lower than published buyback terms.

5. Minimum Investment Accessibility

Lower minimums score higher for accessibility. This dimension matters more for investors with smaller rollover balances; investors moving substantial employer-plan funds may find higher-minimum companies' service models more appropriate.

6. Independent Ratings & Operational History

BBB rating, BCA rating, years in business, and material regulatory or legal actions in the last 5 years. Companies are evaluated on present-day operations, but historical issues are disclosed openly in each profile.

The 2026 Regulatory Landscape: What Recent Federal Action Means for Gold IRA Investors

On August 7, 2025, President Trump signed an Executive Order titled "Democratizing Access to Alternative Assets for 401(k) Investors." The Order directs the Department of Labor to reexamine its guidance on alternative assets — including private equity, real estate, commodities, and digital assets — within ERISA-covered 401(k) plans.

The author's reading of this Order, informed by published commentary from ERISA-focused law firms, is summarized below. Investors making decisions based on the Order's implications should consult an ERISA-qualified specialist.

What the Order does: It directs the DOL to clarify positions on alternative assets and the appropriate fiduciary process associated with offering asset allocation funds containing investments in alternative assets. It marks a shift away from Biden-era guidance that discouraged alternative assets in 401(k)s.

What the Order does not do: The Executive Order sets policy direction, but it does not alter fiduciary obligations under ERISA. The Order does not change the rules governing self-directed IRAs (including Gold IRAs), nor does it create any new documentation requirement for Gold IRA companies facilitating rollovers.

IRS Publications 505 and Schedule D — part of the regulatory framework governing self-directed retirement accounts. Photo: Kelly Sikkema / Unsplash

What it means for Gold IRA investors: The broader policy direction is one of expanding, rather than restricting, access to alternative assets within retirement frameworks. For investors considering a 401(k) rollover into a self-directed Gold IRA, the rollover mechanics themselves remain unchanged — but the policy environment around alternative assets in retirement planning is shifting in a direction that may make these conversations more common in 2026 and beyond.

The author's view: regardless of regulatory direction, a 401(k) rollover decision is a meaningful financial planning event that benefits from professional guidance. Investors should consult a licensed financial advisor or ERISA-qualified specialist before initiating a rollover from an employer-sponsored plan into any self-directed IRA structure.

Practical considerations for any 401(k) rollover

Whether the rollover is in your best interest. This is a personal financial planning question that depends on your overall retirement strategy, current employer-plan options, tax situation, and time horizon.

Direct vs. indirect rollover mechanics. Direct rollovers (trustee-to-trustee transfers) avoid the mandatory 20% withholding that applies to indirect rollovers. Most reputable Gold IRA companies default to direct rollovers; confirm this in writing before proceeding. For a full walkthrough of the 60-day rule, transfer mechanics, and one-rollover-per-year limit, see our complete gold IRA rollover guide.

Custodian independence. The Gold IRA company is not the IRS-approved custodian holding your account; that is a separate entity. A registered precious metals dealer is not a custodian; your IRA is held by a regulated custodian.

IRS-approved metals only. Not all precious metals qualify for IRA inclusion. IRS Publication 590-A and 590-B specify purity standards (gold .995 minimum, silver .999 minimum, platinum and palladium .9995 minimum), with the American Gold Eagle qualifying under a statutory exception.

Augusta Precious Metals: Best for Education-First Buyers and Larger Rollovers

Augusta Precious Metals operates an education-first model in the Gold IRA market. Before any sales interaction occurs, prospective clients are offered a one-on-one web conference led by Devlyn Steele, a Harvard-trained economic analyst. This pre-sales educational commitment differentiates Augusta from competitors who move directly to account-opening discussions.

This guide does not constitute investment, tax, or legal advice. For guidance specific to your financial situation, consult a licensed financial advisor or ERISA-qualified plan specialist.

Augusta Precious Metals — Verified Operational Data

Depository: Delaware Depository, with Lloyd's of London insurance

Fee disclosure: Setup $50 (often waived), $100/year custodian, $100/year storage — published in writing before account opening

Years operating: Since 2012

Buyback: Buyback program offered; the company explicitly notes it cannot legally guarantee buybacks

Transparency assessment: Augusta scores highest in the lineup on fee transparency and on the clarity of its single-custodian, single-depository operational stack. Salaried (not commission-based) representatives align advisor incentives with investor outcomes.

Honest trade-off: The $50,000 minimum is the highest among the major Gold IRA companies; investors with less than $50,000 should consider Goldco ($25K minimum) or American Hartford Gold ($10K minimum).

Goldco: Best for 401(k) and Traditional IRA Rollovers

Goldco's core operational competency is the rollover process — specifically helping clients transition funds from existing 401(k), 403(b), and traditional IRA accounts into a self-directed Gold IRA. The company's customer service infrastructure is organized around rollover-specific clients.

Goldco — Verified Operational Data

Minimum investment: $25,000

BBB rating: A+ (accredited since 2011)

BCA rating: AAA

Custodians: STRATA Trust and Equity Trust

Depositories: Brink's Global Services and Delaware Depository

Years operating: Founded in 2012 in Calabasas, California

Buyback: Buyback guarantee offered with claimed first-right-of-refusal pricing

Transparency assessment: Goldco discloses custodian and depository partners openly and offers segregated and non-segregated storage with clear pricing differentials. Fee structure is published.

Honest trade-off: Like most dealers, Goldco earns money on spreads — the difference between wholesale and retail metal prices. Reviews occasionally mention higher markups on specialty or proof coins compared to simple bullion. Investors should request product-specific pricing and stick to bullion coins for the tightest spreads.

Birch Gold Group: Best for Long Operational Track Record and Custodian/Depository Optionality

Birch Gold Group has been in the Gold IRA space since 2003, making it the longest-tenured company in this evaluation. The company has reportedly helped over 40,000 customers since 2011.

Birch Gold Group — Verified Operational Data

Minimum investment: $10,000

BBB rating: A+ (4.63/5 average across 197+ customer reviews)

BCA rating: AAA

Custodians: GoldStar Trust Company and Equity Trust Company (Birch does not provide its own custodial services)

Depositories: Brink's Global Service, Delaware Depository, Texas Precious Metals Depository, International Depository Services, and Texas Bullion Depository

Fee disclosure: $100/year custodian fee (Equity Trust or STRATA Trust), $100/year storage; Birch does not add fees on top of custodian charges

Years operating: Since 2003 — one of the longer-running Gold IRA dealers

Buyback: Buyback program offered; unlike Goldco, Birch does not offer a formal buyback guarantee

Transparency assessment: Birch provides the broadest depository optionality in the lineup — five named IRS-approved depositories spanning Delaware, Texas, and Nevada — which is meaningful for investors who want geographic diversification of physical storage. Custodian partnerships are clearly disclosed.

Honest trade-off: Fee drag is significant on smaller accounts; investors with balances under $25,000 should compare total all-in fee burden carefully against flat-fee alternatives.

American Hartford Gold: Best for Accessibility and Lowest Combined Entry Cost

American Hartford Gold launched in 2015 in Los Angeles and has grown rapidly, earning an A+ BBB rating in under a decade.

American Hartford Gold — Verified Operational Data

Fee disclosure: $180/year flat storage, no setup fee

Years operating: Since 2015

Buyback: Buyback program with published price-match protection

Promotional: Up to $15,000 free silver promotion on qualifying purchases

Transparency assessment: AHG offers the cleanest entry-cost structure in the lineup — no setup fee plus a flat-rate storage fee creates the most predictable first-year cost profile. Single-depository relationship simplifies the operational stack.

Honest trade-off: Shorter operational track record than Augusta, Goldco, Birch, or Rosland. The promotional structure (free silver on qualifying purchases) means total cost depends on product pricing, which should be confirmed in writing before commitment.

Noble Gold Investments: Best for Texas Storage and Smaller-Account Service

Noble Gold Investments distinguishes itself within the lineup through a specific operational feature: Texas depository access via the IDS Texas vault, alongside Delaware Depository as a standard option.

Noble Gold Investments — Verified Operational Data

Minimum investment: $20,000

BBB rating: A+

BCA rating: Contact company

Custodian: Equity Institutional

Depositories: IDS Texas vault and Delaware Depository

Fee disclosure: Contact company for current fee schedule

Distinctive product: Royal Survival Pack option — segregated physical metals separate from the IRA structure, for investors seeking direct ownership alongside their retirement account

Transparency assessment: Noble Gold's named Texas depository relationship is a verifiable operational differentiator, not a marketing claim. Single-custodian relationship simplifies the operational stack.

Honest trade-off: Total all-in fee data is less comprehensively published than Augusta or Goldco; investors should request a complete written fee schedule before account opening.

Preserve Gold: Best for New-Investor Accessibility with Established Custodian Relationships

Preserve Gold is the newest entrant in this evaluation, founded in 2022 and headquartered in Scottsdale, AZ. The company has accumulated favorable third-party ratings in its first four years of operation while partnering with the same established custodians and depositories as longer-tenured competitors.

Preserve Gold — Verified Operational Data

Minimum investment: $10,000 reported by most independent sources; confirm with the company directly

BBB rating: A+ with approximately 4.96/5 customer review average

BCA rating: Contact company

Custodians: Equity Trust, GoldStar Trust, and Horizon Trust

Depositories: Delaware Depository, International Depository Services, and Texas Precious Metals Depository

Legal status: No significant government actions or class-action lawsuits identified in current records

Transparency assessment: Preserve Gold partners with three named custodians and three named depositories — meaningful operational optionality openly disclosed. Fee structure is documented in published reviews and confirmed by company representatives on request.

Honest trade-off: Operating since 2022, Preserve Gold has the shortest track record in this lineup. Investors prioritizing multi-decade operational history will reasonably weight this factor toward longer-tenured alternatives.

Rosland Capital: Considerations for Specialty Coin Inventory with Transparency Caveats

Rosland Capital occupies a specific niche in the precious metals market through exclusive specialty coin partnerships with Formula 1, the PGA Tour, and the British Museum. This positions Rosland differently from competitors focused primarily on standard bullion.

Rosland Capital — Verified Operational Data

Minimum investment: $10,000 for IRAs; $2,000 minimum for direct purchases

Years operating: Since 2008, headquartered in Los Angeles with international offices in Hong Kong, London, Germany, and Sweden

Transparency assessment: Rosland scores well on independent ratings (A+/AAA), custodian/depository disclosure (named partners), and longevity. However, on the Fee Transparency dimension specifically — the lead criterion in this methodology — Rosland has documented concerns that investors should weigh carefully.

Honest concerns to consider: Rosland's variable 3%–33% commission range has been documented as creating uncertainty, and multiple customer complaints cite confusion over pricing and feeling overcharged. Some customer feedback also highlights issues with communication and delays, particularly during the buyback process.

The author's view: Rosland is a legitimate, established Gold IRA company with strong consumer-protection agency ratings. However, the documented pricing transparency concerns are exactly the kind of operational signal this methodology is designed to surface. Investors prioritizing fee predictability should request — and require — a complete written fee schedule including any commission ranges before opening an account. Investors prioritizing specialty coin inventory may find Rosland's offering distinctive enough to justify the additional due diligence required.

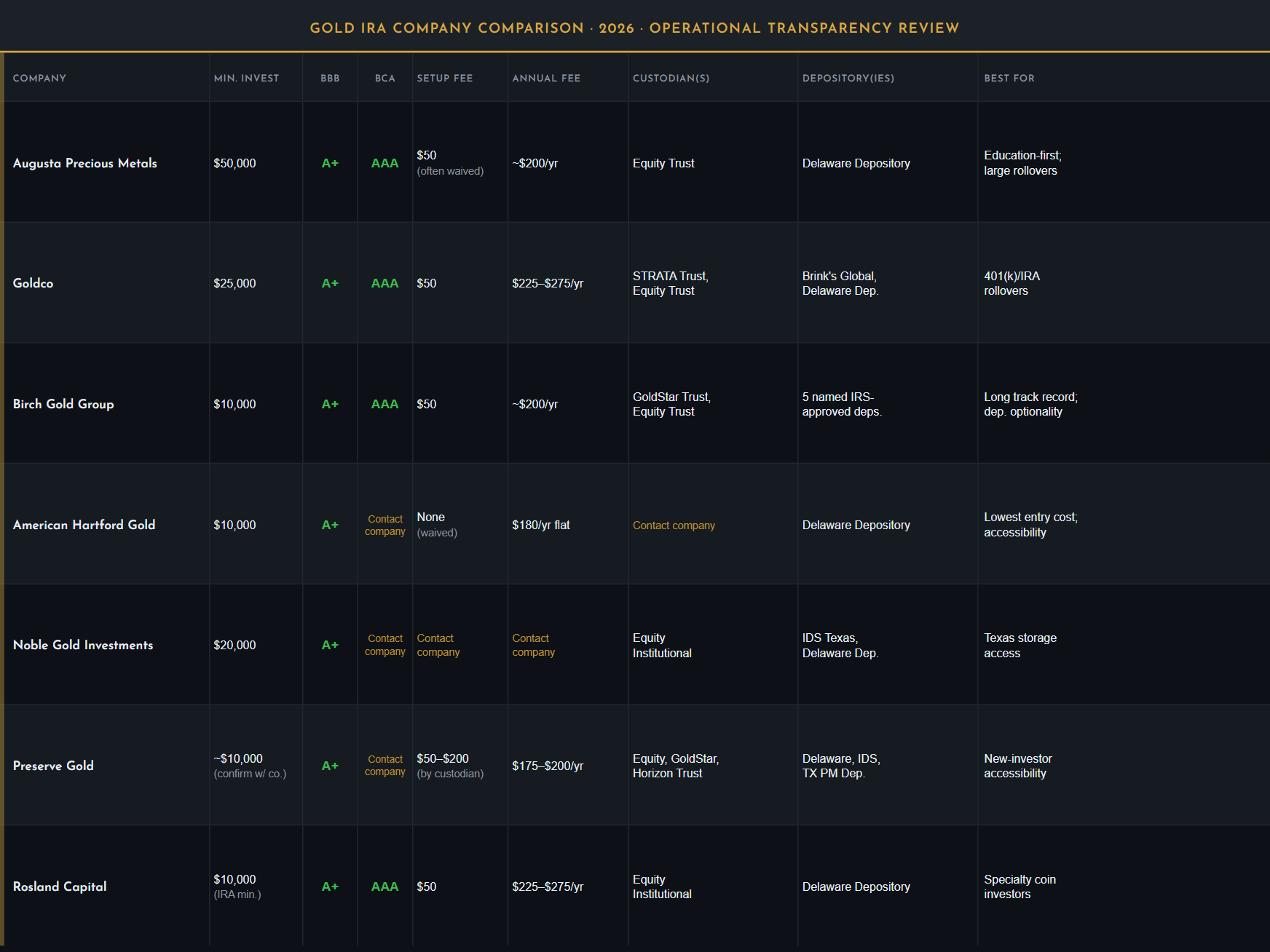

Gold IRA Company Comparison: 2026 Summary

2026 Gold IRA company comparison across nine operational transparency dimensions — seven companies. Setup and annual fees vary by account size and custodian; contact companies directly to confirm current fee schedules. Amber cells indicate data not publicly disclosed — contact company to verify. BCA = Business Consumer Alliance. Ratings subject to change. Chart: Vault Retirement Guide

Gold IRA vs. Physical Gold: Understanding the Difference

A Gold IRA holds IRS-approved precious metals through a self-directed IRA custodian, with the metals stored in an IRS-approved depository — not in the account holder's physical possession. Physical gold purchased outside an IRA has different tax treatment, storage considerations, and liquidity characteristics.

For retirement planning purposes, the Gold IRA structure preserves the tax-advantaged nature of IRA contributions and rollovers. Physical gold outside an IRA is a taxable asset subject to capital gains treatment upon sale. Investors comparing these options are typically choosing between distinctly different goals: retirement tax deferral (Gold IRA) versus direct ownership and immediate liquidity (physical gold outside a retirement account).

The choice is not exclusive — investors can hold both, recognizing that each serves a different purpose within an overall asset allocation strategy. Investors new to the Gold IRA structure can find a full explanation of IRS rules, contribution limits, and approved metals in our gold IRA fundamentals guide.

Red Flags: What to Watch for When Evaluating Gold IRA Companies

Not all Gold IRA companies operate to the same operational transparency standard. The warning signs below distinguish companies built around informed-consent transparency from companies built around aggressive sales conversion:

No written fee schedule before account opening. Reputable companies provide a complete, itemized fee disclosure — setup fees, annual storage fees, annual custodial fees, any wire or transaction fees — before asking for any commitment. Providers that disclose fees only after the account-opening process is initiated should be treated with caution.

Vague or undisclosed custodian relationships. Your metals are held by an independent IRS-approved custodian, not the Gold IRA company itself. Companies that are unwilling to name their custodian partners — or that imply they handle custody themselves — introduce structural opacity into a process that should be fully transparent.

Undisclosed depository. A reputable Gold IRA company will name the specific IRS-approved depository or depositories where your metals will be stored. Companies that defer this disclosure until account opening, or that change depository partners without notice, fail the operational transparency test.

Pressure to roll over your entire retirement account. Allocation to precious metals is a diversification strategy, not a total-portfolio replacement. Any company recommending a 100% precious metals IRA allocation is not operating in the investor's best interest.

Unwillingness to discuss the broader rollover decision. A reputable Gold IRA company facilitating a 401(k) rollover should be willing to discuss the considerations involved in moving funds out of an employer-sponsored plan — and to suggest the investor consult a licensed advisor for personalized guidance. Companies that treat a 401(k) rollover as a routine transaction without acknowledging the personal financial planning dimension may not be aligned with long-term investor interests.

Claims of guaranteed returns or "safe" investment. Gold prices fluctuate. No precious metals investment is guaranteed. Companies that imply otherwise are not providing accurate disclosures.

"Home storage IRA" marketing. Home storage for precious metals IRAs is prohibited by IRS rules. Metals must be held at an IRS-approved depository. "Home storage IRA" schemes claiming otherwise violate regulations and trigger immediate taxation. Any company marketing this option should be avoided.

How to Open a Gold IRA: A Step-by-Step Overview

Select a Gold IRA company that meets your minimum investment threshold, your fee transparency standard, and your custodian/depository preferences. Confirm the company will provide a complete written fee schedule before account opening.

Confirm the custodian. The Gold IRA company will work with one or more IRS-approved custodians. Review the custodian's own fee schedule independently — these fees flow to the custodian, not the dealer, and are a separate cost layer.

Open a self-directed IRA account through the chosen custodian. This is a separate account from any existing traditional or Roth IRA you hold.

Fund the account. Options include a direct rollover (for employer plans like 401(k) and 403(b)), an IRA transfer (for existing IRAs), or a cash contribution subject to 2026 IRA contribution limits ($7,500 standard; $8,600 for age 50+ with the additional $1,100 catch-up contribution). Rollover amounts from qualifying employer plans are not subject to annual contribution limits. For mechanics, the 60-day rule, and the one-rollover-per-year limit, see our step-by-step Gold IRA rollover guide for 2026.

Select IRS-approved metals. Your Gold IRA company will provide a product menu of qualifying metals meeting IRS purity standards (gold .995 minimum, silver .999 minimum, platinum and palladium .9995 minimum, with the American Gold Eagle qualifying under a statutory exception).

Confirm depository storage. Your metals will be stored at an IRS-approved depository. Confirm whether storage is segregated (your specific metals stored separately under serial-number tracking) or commingled (pooled with other investors' metals). Segregated storage typically costs approximately $50/year more.

2026 IRA & 401(k) Contribution Limits (Reference)

IRA Standard

$7,500

Under age 50

IRA Age 50+ Catch-Up

$8,600

Age 50+ per year

401(k) Standard

$24,500

All ages

401(k) Age 50+

$32,500

Total including catch-up

Frequently Asked Questions About Gold IRA Companies

Which Gold IRA company has the lowest minimum investment?

Among the seven companies evaluated in this guide, American Hartford Gold, Birch Gold Group, Preserve Gold, and Rosland Capital all offer $10,000 minimums for IRA accounts. Augusta Precious Metals has the highest minimum at $50,000, with Goldco at $25,000 and Noble Gold at $20,000 occupying the middle tier.

Which Gold IRA company is best for education?

Augusta Precious Metals operates the most structured education model in this lineup. The company offers a pre-purchase one-on-one web conference led by Devlyn Steele, a Harvard-trained economic analyst, before any account-opening discussion takes place. This pre-sales educational step is not replicated by other evaluated companies in this guide.

How does ERISA apply to a Gold IRA rollover?

ERISA (the Employee Retirement Income Security Act) primarily governs employer-sponsored retirement plans such as 401(k) and 403(b) accounts. Once funds are rolled over from an ERISA-covered plan into a self-directed Gold IRA, the receiving IRA is generally not subject to ERISA's fiduciary framework — IRAs are governed by separate provisions of the Internal Revenue Code. The August 2025 Executive Order on alternative assets in 401(k) plans does not change this structure or create new documentation requirements for Gold IRA companies. However, the rollover transaction itself is a significant financial decision, and investors may benefit from consulting a licensed financial advisor or ERISA-qualified specialist before initiating a rollover from an employer plan. This is general informational content and not legal or financial advice.

What fees should I expect with a Gold IRA?

Gold IRA fees typically include account setup fees ($0–$100, sometimes waived), annual custodian fees ($75–$150 depending on the custodian), and storage and insurance fees ($100–$200 per year, varying by depository and whether storage is segregated). Many companies also embed dealer spreads (markups) in the purchase price of coins and bars; this is how dealers earn revenue beyond stated fees. Always request a complete written fee schedule before opening an account, and ask specifically about product premium over spot price.

What is the difference between a Gold IRA and physical gold?

A Gold IRA holds IRS-approved precious metals inside a self-directed IRA structure, preserving tax-advantaged treatment for retirement planning purposes. Physical gold purchased outside an IRA is a taxable asset subject to capital gains tax upon sale. The Gold IRA structure is designed for long-term retirement diversification and tax deferral; physical gold outside an IRA offers direct ownership and immediate liquidity but without the tax advantages of the IRA wrapper.

What gold types are approved for an IRA?

The IRS requires gold held in an IRA to meet a minimum purity of .995 (99.5% pure). Approved forms include certain gold bars and rounds meeting LBMA standards, and specific government-minted gold coins such as American Gold Eagles (qualifying under a statutory exception at .9167 purity) and Canadian Gold Maple Leafs. Collectible coins and most numismatic items do not qualify. Your Gold IRA company and custodian should provide a qualifying-metals list before any purchase.

What happens to my Gold IRA if the company goes out of business?

Your Gold IRA assets are held by your custodian and stored at an independent IRS-approved depository — they are not held by the Gold IRA company itself. If a Gold IRA company ceases operations, your metals remain with the custodian and depository. You would work directly with the custodian to either maintain the account or transfer assets to another approved provider.

Is a Gold IRA a good investment in 2026?

A Gold IRA is a diversification strategy, not a guaranteed-return investment. Gold prices fluctuate and may decline. For investors seeking to diversify a retirement portfolio away from pure equity and fixed-income exposure, a precious metals IRA allocation may serve a hedging role — but appropriate allocation size depends on individual risk tolerance, time horizon, and existing portfolio composition. The author's view is that 5–15% allocation ranges are commonly cited by financial educators, but no allocation guidance in this guide constitutes personalized advice. Consult a licensed financial advisor before making any allocation decision.

What is a good Gold IRA?

A good Gold IRA holds IRS-approved gold (.995 fineness minimum per IRC §408(m)) through an IRS-approved custodian, with metals stored at an approved depository — home storage constitutes a taxable distribution (McNulty v. Commissioner, T.C. 2021-84). Quality signals: complete written fee disclosure before account opening, named custodian and depository partners, and verifiable BBB and BCA ratings. The 2026 contribution limit is $7,500 ($8,600 for age 50+).

Who is the most reputable Gold IRA company?

No single company holds universal claim to that distinction. Reputable providers share verifiable signals: A+ BBB accreditation, AAA BCA rating, a complete written fee schedule published before account opening, a named IRS-approved custodian, a named IRS-approved depository, and documented buyback terms. Longer operational history provides more track record to evaluate. Our 2026 comparison evaluates seven companies on these dimensions.

What are the tax implications of a Gold IRA rollover?

A direct (trustee-to-trustee) transfer triggers no taxable event — funds retain their tax-advantaged status. An indirect rollover requires redeposit within 60 calendar days; missing that deadline makes the full amount ordinary income, plus a 10% early-withdrawal penalty if you are under 59½. The one-per-12-months limit under IRC §408(d)(3)(B) restricts indirect rollovers across all your IRAs. Source: IRS Publication 590-A.

Compare Your Options Before You Commit

Request information kits from at least two companies. Compare written fee schedules side-by-side. Ask each company to name its custodian and depository partners before committing to anything.

⚠ Not Financial Advice. We may receive compensation if you request information through links on this site. See full disclosure below.

Not Financial Advice

All content on this website is for general informational and educational purposes only. Nothing here constitutes financial, investment, tax, or legal advice. Company profiles are for informational comparison only and do not constitute an endorsement or recommendation to use any specific company's services.

Affiliate Disclosure (FTC Compliance)

This site may receive compensation from partner companies when visitors request information through links on this page. Compensation may influence which companies are featured, but not the accuracy of factual information. Disclosed per FTC 16 CFR Part 255.

Accuracy & Currency

Company data (minimums, fees, ratings) was last verified on 2026-05-16. Fee structures, minimum investments, and company standings change over time. Always verify current information directly with each company before making any commitment.

No Guarantees

Past performance of any precious metals company or the metals they sell does not guarantee future results. BBB ratings and BCA ratings reflect historical consumer data and may change. Conduct your own due diligence before selecting any financial services provider.